An Overview of Agentic Payment | New Protocols, PSPs and Checkout Flow

- Gianluca Luke Caccamo

- Dec 3, 2025

- 11 min read

Updated: Dec 31, 2025

Since the adoption of AI, the global payment service provider (PSP) sector is undergoing one of its broadest transformations since the early e-commerce boom. Multiple forces—AI automation, programmable money, stablecoins, and agentic commerce—are reshaping how payments are routed, authorized, and monetized at both consumer and enterprise levels.

PSP Market Overview

The global PSP market in 2025 is estimated at roughly USD 62.82 billion and is projected to grow at over 10% CAGR through 2033, driven by digitization, regulation favoring cashless economies, and the rise of instant payments such as Pix in Brazil and UPI in India.

According to McKinsey’s 2025 Global Payments Report, payment flows generate over USD 2.5 trillion in revenue on more than 3.6 trillion transactions worldwide, with payments remaining one of the most profitable segment in financial services.

Payment revenue composition is shifting toward low-yield, instant, and account-to-account (A2A) channels, pushing PSPs to capture value via embedded services such as acquiring, working-capital automation, fraud analytics, and context-aware routing.

Structural Shifts Shaping PSP Strategy

Three fundamental shifts are redefining payments:

Fragmentation and regionalization: Local schemes like Bizum in Spain and Pix in Brazil are becoming powerful alternatives to global card networks, emphasizing sovereignty and interoperability within economic blocs such as the EU and Latin America.

Tokenized and programmable money: Stablecoin adoption is accelerating as regulatory clarity grows in the US, EU, UK, and Japan. PSPs capable of integrating digital assets alongside fiat rails—like PayPal’s USD-backed tokens—will gain advantage.

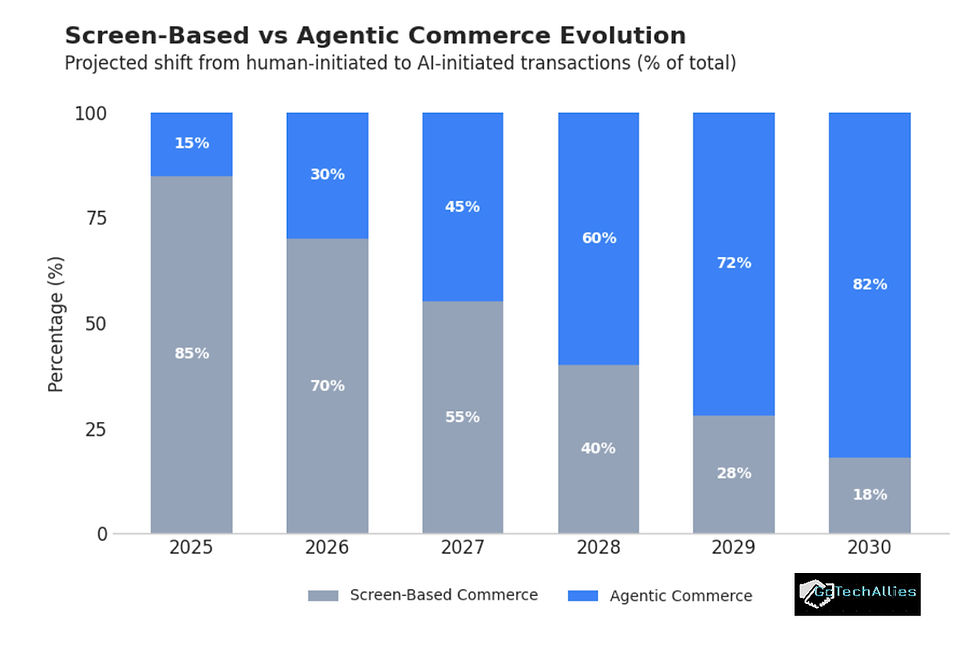

Agentic AI and automation: Payments are moving from human-initiated to AI-initiated flows, where large language models (LLMs) or autonomous agents complete purchases, manage budgets, and handle B2B settlements on behalf of users. In an agentic payment environment, PSPs need agent identity layers (KYAI: Know Your Agent’s Intent), programmable consent frameworks, and context-aware orchestration capable of real-time, autonomous decisions.

What “agentic payments” mean

Agentic payments require AI agents autonomously making purchases, subscriptions, bookings or payments on behalf of a user. That breaks assumptions in today’s payment stack (human click + device/browser + cardholder present flows) and creates new requirements: automated authority/delegation (mandates), strong authentication & attestation (prove the agent is authorized), improved risk/fraud controls, new APIs & standards for agent-to-merchant interactions, and potentially new liability/merchant-of-record models. Google’s AP2 work and the Stripe/OpenAI Agentic Commerce work are explicit efforts to provide those building blocks.

Technical primitives PSPs & infrastructure must provide for agentic payments

Mandates / agent credentials — machine-readable delegation that limits what an agent may do (scope, spend caps, merchant allowlists).

Agent attestation & auth — cryptographic proof an agent is acting under the user’s authority.

Tokenization + vaulting + escrow patterns — to avoid giving agents direct access to raw funds/cards.

Risk & compliance hooks — real-time rules, fraud scoring, KYAI for merchants and agents.

Platform/connect features — split payouts, marketplace flows, MOTO (mail/phone order) or new agent flows for platforms (Stripe Connect/Adyen Marketplace).

Major Players in Agentic Payments

Stripe — public sessions and developer activity around agentic commerce + strong Platform/Connect ecosystem. Very developer-friendly, already integrated into early agentic commerce pilots (existing partnership with OpenAI). Good for merchants that want to adopt open standards and developer APIs.

PayPal — issuing developer toolkits and partnering with agentic platforms (Perplexity, etc.). Large account base and existing user consent/checkout flows make PayPal attractive for consumer-facing agent experiences.

OpenAI - with its 800 million weekly active users, the platform provides the perfect playground to test agentic payments and the recent partnership with Stripe signal this intent.

Card networks & cloud initiatives (Visa/Mastercard tools, Google AP2) — focusing on standards and secure attestation/mandates; these groups will shape interoperability and liability models. Google’s AP2 and consortia activity show ecosystem-level standardization is already underway.

Agent-native startups (Payman, Skyfire, etc.) — explicitly build rails, identity, escrow and agent-safe spend primitives. These are the earliest vendors whose products are designed around the threat model/UX of AI agents. They often integrate to existing PSPs and card rails for settlement.

Regional players / rails — examples like Razorpay + NPCI pilots in India show national rails can enable agentic payments quickly where real-time rails (UPI) already exist. Expect country-level differences

Agentic Payment Protocols: A Structured Comparison

Between April and October 2025, the payments industry witnessed an unprecedented wave of protocol launches designed to enable secure, autonomous AI agent transactions. Six major frameworks have emerged, each addressing different layers of the agentic commerce stack with distinct technical architectures and strategic positioning.

Overview of Protocol Launches

The timeline reveals a competitive race driven by platform control and new revenue opportunities:

April 2025 marked the first wave with Mastercard Agent Pay and PayPal Agent Toolkit, both emphasizing integration with existing payment infrastructure and tokenization frameworks.

September 2025 brought the most significant announcements: OpenAI and Stripe's Agentic Commerce Protocol (ACP) launched alongside Google's Agent Payments Protocol (AP2), with PayPal immediately partnering with Google to support AP2 across its ecosystem.

October 2025 saw the card networks respond with Visa's Trusted Agent Protocol (TAP), developed with Cloudflare and designed for merchant-side agent verification.

Throughout this period, Coinbase's x402 protocol matured as the dominant framework for crypto-native, machine-to-machine microtransactions.

Core Architectural Differences

Agent Commerce Protocol (ACP)

ACP signed between OpenAI & Stripe prioritizes developer velocity and transaction execution. Built around Shared Payment Tokens (SPT) and REST APIs, it enables merchants to accept agent-initiated purchases with as little as one line of code. The protocol powers "Instant Checkout" within ChatGPT, allowing users to complete purchases without leaving the AI interface. ACP is explicitly designed to make AI agents a new sales channel, with merchants remaining the merchant of record throughout.

Agent Payments Protocol (AP2)

AP2 (Google) takes a governance-first approach focused on authorization, authenticity, and accountability. Its defining innovation is a three-mandate cryptographic system: Intent Mandates capture user instructions, Cart Mandates record approved purchases, and Payment Authorizations provide network-level visibility. This creates a tamper-proof audit trail suitable for both real-time (human-present) and delegated (human-absent) transactions. Built as an extension of Agent2Agent (A2A) and Model Context Protocol (MCP), AP2 is payment-agnostic and designed for cross-platform interoperability.

Visa Trusted Agent Protocol (TAP)

TAP focuses on me4rchant-side trust and bot differentiation. Using cryptographic signatures based on HTTP Message Signature standards, TAP enables merchants to verify that incoming traffic is from a Visa-approved agent rather than malicious bots. The protocol's key advantage is no-code merchant adoption—verification happens at the CDN layer with no changes to existing checkout flows. Visa maintains a registry of trusted agents, effectively acting as a "guest list" for AI commerce.

Mastercard Agent Pay

Mastercard Agent Pay emphasizes network-level tokenization and traceability. The framework introduces Agentic Tokens—dynamic, cryptographically secured credentials that replace card numbers in agent transactions. A "Know Your Agent" (KYA) registration process ensures only verified agents can transact on the Mastercard network. Like TAP, Agent Pay offers a no-code path via Web Bot Auth at the CDN layer, making adoption accessible to merchants of all sizes.

Paypal Agent Toolkit

PayPal Agent Toolkit leverages account-based trust and existing infrastructure. Rather than building new protocols from scratch, PayPal enables agents to transact through familiar PayPal and Braintree account flows, backed by 25+ years of fraud detection systems. The toolkit includes MCP server integration and supports AP2, positioning PayPal as a bridge between legacy payment rails and agentic commerce.

Coinbase x402

x402 represents a fundamentally different model: autonomous, crypto-native microtransactions. Built on the dormant HTTP 402 "Payment Required" status code, x402 enables AI agents to pay for API calls, data, or computing resources instantly using stablecoins (primarily USDC on Base). Transactions settle in under two seconds with fees below $0.0001, enabling sub-cent pricing impossible with traditional rails. Unlike fiat-focused protocols, x402 assumes fully autonomous agents operating without human presence.

Protocols Strategic Positioning

Transaction-focused protocols (ACP, x402) prioritize frictionless checkout experiences and immediate merchant adoption. ACP targets conversion optimization within AI interfaces, while x402 unlocks pay-per-use API monetization.

Governance-focused protocols (AP2, TAP, Agent Pay) emphasize trust infrastructure, dispute resolution, and regulatory compliance. AP2's mandate system and TAP's agent registry provide the legal and technical foundations for large-scale autonomous commerce.

Infrastructure-focused protocols (PayPal, Mastercard) leverage existing network effects and fraud systems, reducing merchant risk and accelerating adoption through familiar integration patterns.

Interoperability and Convergence

All six protocols share common design principles: agent identity attestation, short-lived tokens or cryptographic receipts, fraud signals adapted for automated behavior, and developer-friendly tooling. Importantly, they are designed to interoperate rather than compete directly:

AP2 explicitly integrates with A2A and MCP standards, positioning itself as middleware compatible with other protocols

TAP is built for compatibility with ACP and x402, with Visa partnering with Coinbase on crypto interoperability

Mastercard Agent Pay supports MCP, A2A, and ACP integration for merchants seeking deeper functionality

x402 has an official A2A extension (the "x402" addition to AP2) for crypto payments within multi-agent workflows

This suggests the ecosystem is converging toward layered specialization: ACP and x402 handle transaction execution, AP2 provides governance and intent verification, and TAP/Agent Pay deliver network-level trust and fraud prevention.

Payment Method Coverage

The protocols divide into fiat-focused (ACP, TAP, Agent Pay, PayPal) and crypto-native (x402) frameworks, with AP2 serving as the only truly payment-agnostic bridge supporting cards, real-time bank transfers, digital wallets, stablecoins, and cryptocurrencies. This positions Google's AP2 as the most comprehensive governance layer for heterogeneous payment ecosystems.

Adoption Trajectory

ACP has the strongest early traction through ChatGPT integration, with Etsy merchants live in the US and Shopify soon to follow suit. AP2 boasts the broadest coalition with 60+ partners including PayPal, Adyen, American Express, Coinbase, and UnionPay. TAP and Agent Pay leverage the scale of Visa and Mastercard networks, ensuring global reach once adoption scales. x402 dominates crypto-native use cases, with Coinbase's AgentKit providing native integration.

Implications for the Payments Ecosystem

The strategic takeaway is that no single protocol will dominate. Instead, the ecosystem is fragmenting into complementary layers:

Checkout/UX layer: ACP (fiat), x402 (crypto)

Governance/compliance layer: AP2 (universal), TAP (Visa), Agent Pay (Mastercard)

Infrastructure layer: PayPal (account-based), card networks (tokenization)

PSPs will need multi-protocol support to serve merchants across different agent ecosystems. Those integrating ACP, AP2, and network-level protocols (TAP or Agent Pay) will be best positioned to capture agentic commerce volume across screen-based and screenless environments.

How PSPs and Payment Buttons Fit into the Current, Screen-Based (Chatbots, Copilots) Human-Initiated AI Commerce

Right now, “agentic commerce” is mostly human-in-the-loop.

Users are still on a screen (mobile, desktop, chat), interacting with an AI (ChatGPT, Perplexity, Copilot, etc.).

The AI curates options — flights, shoes, software — and surfaces a checkout button or payment link.

The user then authorizes the payment manually, often within a PSP’s hosted UI or embedded SDK.

This makes it compliant with existing payment regulations (since the human still confirms the purchase) but already shifts discovery and cart-building to the AI.

How PSPs Integrate into this Framework: Screen-Based Human-Initiated

PSPs are making small but crucial adaptations to enable AI front-ends to complete payments.

Example: When ChatGPT or Perplexity shows you “Book with Expedia,” the AI is calling PSP APIs (via Expedia or Stripe/Adyen backend) to prepare a payment intent and render a clickable button — the human then approves, but the AI handles the logic of what, where, and how much.

Payment Button in Current Screen-Based Human-Initiated AI Checkout Flow

In this framework, payment buttons are evolving into “AI-ready” components:

Smart deep links — AI agents can generate contextual payment URLs (“Buy this flight → [Stripe Checkout Link]”).

Universal pay buttons — Experiments (e.g., from Google and PayPal) aim to make “Pay” buttons that can be embedded in chat interfaces or result cards.

Persistent credentials — If users authorize wallets (Apple Pay, PayPal, Google Pay), AI tools can suggest and pre-fill them for faster human confirmation.

So far, the big shift isn’t new rails — it’s new orchestration layers between the AI interface and existing PSP APIs.

Example Flow Today (Screen-Based)

User: “Book me a flight to Lisbon this weekend.”

AI: Fetches flight data via APIs, picks the best option.

AI: Calls PSP API (create_payment_intent or checkout_session).

PSP returns a hosted payment link or button.

AI displays it inline (“Tap to pay with Stripe / PayPal”).

User confirms; PSP completes transaction and notifies merchant.

In short: Current AI commerce still uses traditional PSP rails — but AI agents create and present payment flows dynamically, while humans still authorize via payment buttons.The most forward-thinking PSPs (Stripe, PayPal, Adyen) are already evolving their APIs to support when that human confirmation disappears — i.e., fully agentic commerce.

What’s next

Autonomous checkout: AI will handle steps 1–6 without human clicks, using delegated tokens (agent credentials).

Agentic-ready PSPs (Stripe, PayPal, Payman) will expose APIs that allow agents to act within preset limits (spend caps, merchant allowlists).

UI disappears: the “Pay” button becomes a silent confirmation event in the background, governed by user-defined rules.

Strategic Implications

Merchants will rely less on on-site checkout flows and more on headless PSP integrations connected to AI platforms.

PSPs evolve from backend utilities into trusted orchestration and risk partners, managing agentic authentication and audit trails.

Consumers gain frictionless in-context payments, where confirmations occur inside AI chats or app overlays rather than external web redirects.

From Screen-Based to Agentic/Screenless AI Commerce

The shift from screen-based AI commerce to fully agentic (screenless) commerce is arguably the biggest transformation coming to payments since mobile wallets. Let’s unpack how it will change the space — from the user experience to the PSP and infrastructure level.

What “agentic commerce” really means

Instead of the user tapping “Buy,” an AI agent (a digital representative) acts on your behalf — booking, ordering, or subscribing — according to your preferences, budget, and mandates.

No screen, no checkout button — the “buy” event happens automatically, governed by delegated authority and trust frameworks.

Example: Your travel agent-AI knows your travel policies and budget. It books flights and hotels automatically and pays using your pre-authorized agent credentials — you simply get the itinerary and receipt.

What Changes Technically in Screen-less Agentic Commerce

How the Business Model of PSPs Changes

Historically, the Legacy PSP model focused on foundational services: processing card payments and managing the customer checkout user experience (UX). Their revenue largely stemmed from transaction fees on user-initiated payments, with their primary differentiator being merchant UX differentiation—think seamless, fast checkouts.

The future, however, points to the Agent-Native PSP. This new paradigm shifts the core value proposition from simply processing transactions to providing the "trust fabric for autonomous agents to transact safely." This is a critical pivot, anticipating a world where AI and autonomous software agents handle a significant volume of commerce.

The revenue model diversifies significantly, moving beyond simple transaction fees to include Subscription / per-agent access fees, Delegated wallet management, and Compliance services.

This evolution signals that PSPs are transforming from mere payment processors into essential infrastructure providers for the autonomous, AI-driven economy.

Example Flow Tomorrow (Fully Agentic)

You tell your personal AI: “Keep me stocked with coffee beans I like under €25/kg.”

Your agent checks inventories, chooses the best supplier, and pays via an agent credential held at Stripe or PayPal.

No checkout page ever appears.

You receive a push notification: “Coffee ordered — €22.90 via Stripe AgentPay, next delivery Friday.”

Your bank statement reads: “Purchase by Authorized Agent.”

Strategic Implications

Merchants need to expose APIs, not just webshops.

PSPs must authenticate agents, not browsers.

Consumers must manage agent permissions (think: “money firewall”).

Networks must define new liability and dispute rules (who’s responsible if an AI misbuys?).

Author

Gianluca Caccamo connects Leaders with Data for Strategic Partnerships, after more than 15 years at companies like Google, Pinterest and Wix among others. Advising companies on E-commerce, Advertising, Saas and AI Partnerships. [Follow on Linkedin]

Follow on Linkedin ❤️

Sources

https://www.cognitivemarketresearch.com/payment-service-provider-market-report

https://www.mckinsey.com/industries/financial-services/our-insights/global-payments-report

https://www.novalnet.com/blog/agentic-commerce-and-the-future-of-payment-processing/

https://www.omnius.so/blog/leading-fintech-european-startups

https://www.linkedin.com/pulse/how-payment-services-provider-works-one-simple-flow-2025-dhpte

https://www.clearlypayments.com/blog/how-big-is-the-payment-processing-market-by-region-in-2025/

https://www.reportsandinsights.com/report/payment-service-provider-market

https://www.forbes.com/advisor/business/software/best-payment-gateways/

https://thefinancialtechnologyreport.com/the-top-25-payments-companies-of-2025/

https://lawyersafran.com/top-11-payment-service-providers-psps-for-2025/

https://www.eca.europa.eu/ECAPublications/SR-2025-01/SR-2025-01_EN.pdf

https://www.nerdwallet.com/best/small-business/payment-processing-companies

https://www.checkout.com/blog/payment-innovation-drive-revenue

https://www.airwallex.com/eu/blog/payment-processing-industry-statistics

Comments